List To Floor Assertion

Financial Statement Analysis Example Financial Statement Analysis Financial Statement Analysis

9 Assertion Hallway Concepts That Will Deliver The Thoroughfare To Life 2020 In 2020 Living Room Reveal Beach House Decor Hallway Decorating

Pin On Customer Experience

Chapter 9 Audit Procedures

Pin On For Me Resilience

Distinct Furniture Along With Modern Pattern Makes An Assertion In Your Home Come Across Present Day Settees Areas And Me Home Home Remodeling House Interior

The assertion of accuracy and valuation is the statement that all figures presented in a financial statement are accurate and based on proper valuation of assets liabilities and equity balances.

List to floor assertion.

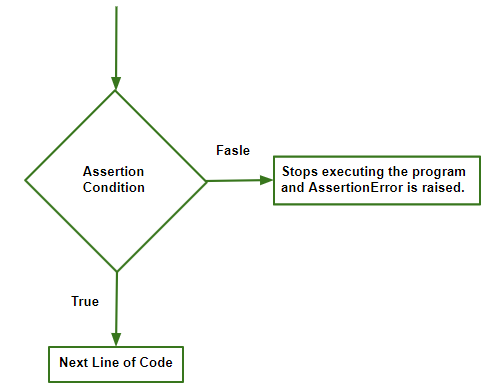

Python Assertion Error Geeksforgeeks

100 Opposite Words List Antonym Vocabulary Example Sentences In 2020 Opposite Words Opposite Words List Vocabulary

A Literary Review Is A Summary About A Specific Topic In Essay Form Contains A Apa Re Argumentative Essay Creative Writing Workshops College Admission Essay

Small Bathroom Design Photos Low Budget Small Bathroom Design Photos Low Budget Small Bathroom In 2020 Budget Bathroom Remodel Bathrooms Remodel Diy Bathroom Remodel

Https Comptroller Defense Gov Portals 45 Documents Fiar Fiar Guidance Pdf

Profit And Loss Statement Self Employed Profit And Loss Statement Statement Template Budgeting Worksheets

Wandfarbe Apricot Flur Gestalten Floraler Teppichl Ufer Decorstyle Entrywaydecor Decorsmall In 2020 Narrow Entryway Decor Foyer Decorating Hallway Designs

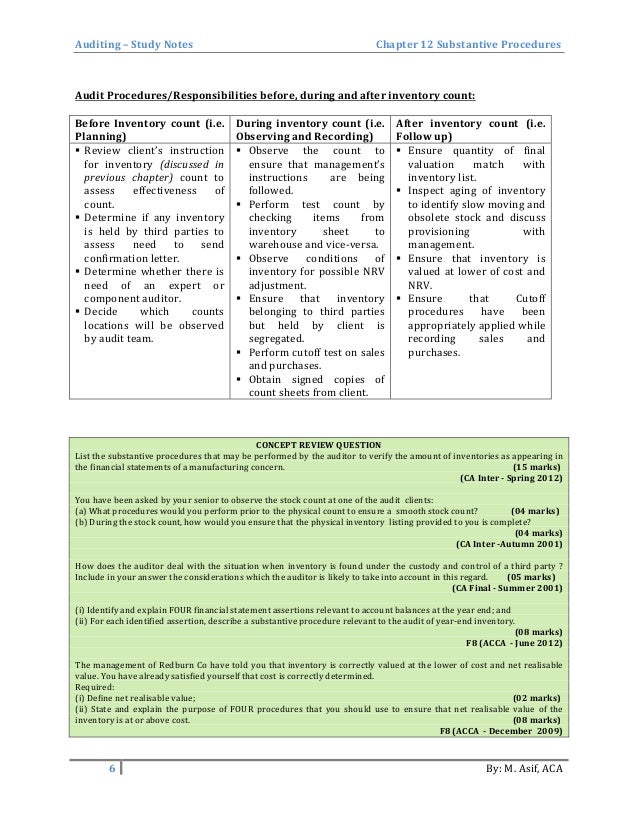

Substantive Procedures Auditing Study Notes

Public Mind Map By Tyler Smith Create Your Own Collaborative Mind Maps For Free At Www Mindmeister Com Mind Map Eos Tyler Smith

Ana Book Blogger On Instagram How Do You Guys Store Your Books Towering Bookshelves Or Stacke In 2020 Study Room Decor Bookshelves In Bedroom Room Ideas Bedroom

Distinct Furnishings Along With Advanced Plan Makes An Assertion In Your Home Look Up New Chairs Mattress And Sto Murphy Bunk Beds Bunk Beds Murphy Bed Plans

A Visit To Rumson Vintage House Plans Luxury House Plans Rumson

Check Out These Out Of This World Approaches With Regard To A Triple Bunk Bed Space Bunkbedcabin Bunk Beds Triple Bunk Beds Modern Bunk Beds

No Ordinary Saugling S Room Baby Room Safari Room Room

100 Laminate Sheets Manufacturers Price List Designs And In 2020 Laminate Sheets Laminate Hardwood

Https Www Acq Osd Mil Pepolicy Pdfs Assertion Package Outline Final Pdf

Red Carpet Birthday Celebration Cubicle Office Birthday Decorations Office Birthday Cubicle Birthday Decorations

Whether Or Not You Want To Make A Bold Assertion Otherwise You Merely Wish To D Bedroom Wallpaper Accent Wall Accent Walls In Living Room Wallpaper Accent Wall

3

Distinct Furniture By Using Contemporary Plan Makes An Assertion In Your Home Find New Chairs Bed Fr Interior Design Home Interior Design Trendy Living Rooms

20 Paulo Coelho Quotes That Will Lift Your Spirit Good Thoughts Quotes Inpirational Quotes Wisdom Quotes

40 Trendy Farmhouse Master Bedroom Design Ideas The Tall White Curtains H In 2020 Farmhouse Style Master Bedroom Stylish Master Bedrooms Rustic Master Bedroom

Promatz Dungeon Floor Theme Terrain Game Mat Flooring Theme Table Games

Dark Sash With Images Interior Design Kitchen Kitchen Interior Mediterranean Kitchen

Source : pinterest.com